Trust and Governance is Not an Afterthought

Why managing AI risk presents new challenges

Aliquet morbi justo auctor cursus auctor aliquam. Neque elit blandit et quis tortor vel ut lectus morbi. Amet mus nunc rhoncus sit sagittis pellentesque eleifend lobortis commodo vestibulum hendrerit proin varius lorem ultrices quam velit sed consequat duis. Lectus condimentum maecenas adipiscing massa neque erat porttitor in adipiscing aliquam auctor aliquam eu phasellus egestas lectus hendrerit sit malesuada tincidunt quisque volutpat aliquet vitae lorem odio feugiat lectus sem purus.

- Lorem ipsum dolor sit amet consectetur lobortis pellentesque sit ullamcorpe.

- Mauris aliquet faucibus iaculis vitae ullamco consectetur praesent luctus.

- Posuere enim mi pharetra neque proin condimentum maecenas adipiscing.

- Posuere enim mi pharetra neque proin nibh dolor amet vitae feugiat.

The difficult of using AI to improve risk management

Viverra mi ut nulla eu mattis in purus. Habitant donec mauris id consectetur. Tempus consequat ornare dui tortor feugiat cursus. Pellentesque massa molestie phasellus enim lobortis pellentesque sit ullamcorper purus. Elementum ante nunc quam pulvinar. Volutpat nibh dolor amet vitae feugiat varius augue justo elit. Vitae amet curabitur in sagittis arcu montes tortor. In enim pulvinar pharetra sagittis fermentum. Ultricies non eu faucibus praesent tristique dolor tellus bibendum. Cursus bibendum nunc enim.

How to bring AI into managing risk

Mattis quisque amet pharetra nisl congue nulla orci. Nibh commodo maecenas adipiscing adipiscing. Blandit ut odio urna arcu quam eleifend donec neque. Augue nisl arcu malesuada interdum risus lectus sed. Pulvinar aliquam morbi arcu commodo. Accumsan elementum elit vitae pellentesque sit. Nibh elementum morbi feugiat amet aliquet. Ultrices duis lobortis mauris nibh pellentesque mattis est maecenas. Tellus pellentesque vivamus massa purus arcu sagittis. Viverra consectetur praesent luctus faucibus phasellus integer fermentum mattis donec.

Pros and cons of using AI to manage risks

Commodo velit viverra neque aliquet tincidunt feugiat. Amet proin cras pharetra mauris leo. In vitae mattis sit fermentum. Maecenas nullam egestas lorem tincidunt eleifend est felis tincidunt. Etiam dictum consectetur blandit tortor vitae. Eget integer tortor in mattis velit ante purus ante.

- Vestibulum faucibus semper vitae imperdiet at eget sed diam ullamcorper vulputate.

- Quam mi proin libero morbi viverra ultrices odio sem felis mattis etiam faucibus morbi.

- Tincidunt ac eu aliquet turpis amet morbi at hendrerit donec pharetra tellus vel nec.

- Sollicitudin egestas sit bibendum malesuada pulvinar sit aliquet turpis lacus ultricies.

“Lacus donec arcu amet diam vestibulum nunc nulla malesuada velit curabitur mauris tempus nunc curabitur dignig pharetra metus consequat.”

Benefits and opportunities for risk managers applying AI

Commodo velit viverra neque aliquet tincidunt feugiat. Amet proin cras pharetra mauris leo. In vitae mattis sit fermentum. Maecenas nullam egestas lorem tincidunt eleifend est felis tincidunt. Etiam dictum consectetur blandit tortor vitae. Eget integer tortor in mattis velit ante purus ante.

The Foundation of Banking AI is Trust and Governance.

There is a version of AI in banking that looks impressive in a demo and fails in production. It surfaces a pricing recommendation with no explanation of how it got there. It makes a lending decision no examiner can reconstruct. It operates across a data environment where nobody is certain what left the perimeter and what didn't.

That version of AI does not get deployed at scale in a regulated institution. It gets killed in the risk committee.

The question for banks isn't whether AI can generate value. At this point, the evidence is overwhelming that it can. The question is whether it can do so in a way that satisfies the OCC, the CFPB, and the SR 26-2 model risk management framework (which superseded SR 11-7). Whether it can be audited after the fact. Whether it can be explained in plain language to a fair lending examiner. Whether the people operating it actually control it.

At ArcOne AI, we believe those requirements aren't constraints on what AI can do in banking. They're the architecture. Trust and governance aren't layered on top of a working system; they're what makes it work.

The Governance Gap Most AI Vendors Ignore

Most AI platforms are built for performance first and compliance second. Explainability is a feature you add. Audit trails are a log configuration. Bias monitoring is a dashboard someone buys later.

That sequencing creates a fundamental problem for banks. Regulated institutions cannot deploy a model they cannot explain, audit, and govern from day one. Retrofitting compliance into a platform that wasn't built for it is expensive, slow, and often structurally impossible. The governance tooling ends up disconnected from the actual decision logic, which means it doesn't satisfy examiners and doesn't give risk teams real visibility.

The result is the pattern we see across the industry: significant AI investment, very few AI deployments actually in production.

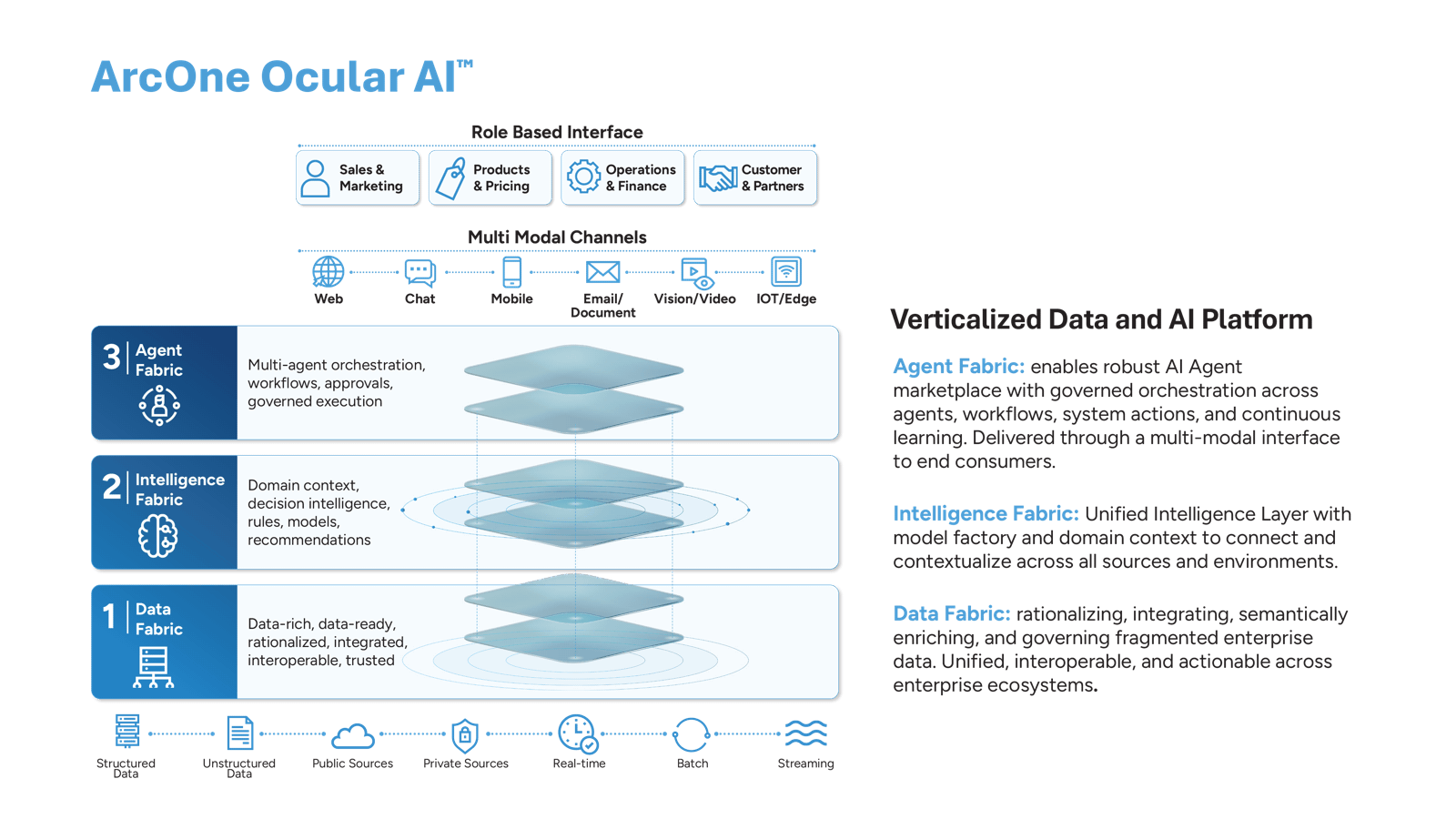

Six Dimensions of Governed AI in Banking

ArcOne BankOS™ is built around six governance pillars that address distinct layers of the trust problem. Each one exists because a real regulatory or operational requirement demands it.

Data & AI Security is the starting point. Before any model runs, the data feeding it needs to be trusted, classified, and secured. ArcOne's Data Fabric enforces security controls at the semantic layer. This means protections travel with the data, not just with the system storing it.

Auditability & Compliance means every action the platform takes is logged, timestamped, and traceable. Every pricing decision, offer, waiver, and exception is part of a complete audit trail. When an examiner asks what happened and why, the answer is retrievable in full and not reconstructed from fragmented logs across multiple systems.

Bias & Fairness is where many platforms stop at good intentions. ArcOne builds active monitoring into the Agent Fabric itself, tracking outputs against fair lending requirements like ECOA and UDAAP, and emerging AI governance standards like ISO 42001. This is continuous, not just at model validation time.

Decision Transparency closes the explainability gap. Every recommendation the system makes includes a plain-language rationale accessible to the people acting on it; relationship managers, operations staff, and examiners alike. There is no black box output that someone downstream must take on faith. It is also what CFPB Circular 2022-03 requires: a black-box model is not an excuse for failing to give the specific reasons behind an adverse credit decision.

Data Quality governs what goes in. The platform's semantic intelligence layer normalizes data across banking cores and applies lineage tracking from source to decision, so the quality of the data underlying any decision is visible and verifiable.

Monitoring & Reporting ensures the system stays governed over time and not just at deployment. Integrated model validation, drift detection, and performance monitoring catch degradation before it becomes a regulatory or business problem.

What a Unified Architecture Actually Means for Governance

Governance in a fragmented architecture is governance theater. You can have an explainability tool, a bias dashboard, and an audit log system that all technically function and still have no coherent view of what your AI is doing across the enterprise.

A unified architecture changes the nature of the problem. When the Data Fabric, the Intelligence Fabric, and the Agent Fabric share a common foundation, governance controls apply consistently across every workflow, every domain, and every decision. There is no gap between what the system does and what the governance layer sees.

This is the design principle behind ArcOne BankOS™. The platform's compliance and governance capabilities aren't modules that sit alongside the core system. They're properties of the infrastructure itself. Lineage tracking, bias monitoring, explainability, and audit logging are built into the domain cartridges, the TERRA orchestration engine, and the 360 application suites. When a new workflow is activated, governance comes with it.

That architecture matters for SR 26-2 compliance, which requires banks to demonstrate ongoing model risk management, not just initial validation. And it matters for the internal trust that determines whether a risk committee will approve a deployment.

The Standard Banks Should Demand

AI that cannot be explained, audited, and governed is not AI you can trust or deploy in a regulated institution. That's not a conservative position. It's a practical one. The cost of a failed deployment, a regulatory action, or a fair lending violation far exceeds the cost of building governance in from the start.

The standard for banking AI should be simple: every decision traceable, every model explainable, every agent accountable. Not as aspirational principles, but as operational properties of the platform.

That is what ArcOne BankOS™ is built to deliver and what we believe every institution evaluating AI should require.

ArcOne BankOS™ is generally available now. To learn more about our governance architecture or schedule a custom demonstration, visit arcone.com.

ArcOne BankOS™, Ocular AI™, LYZA™, TERRA™, IntelliArc™, Enrich360™, Experience360™, and Exceptions360™ are trademarks of ArcOne AI.