Maximizing Offer Management for Retail Banking

Why managing AI risk presents new challenges

Aliquet morbi justo auctor cursus auctor aliquam. Neque elit blandit et quis tortor vel ut lectus morbi. Amet mus nunc rhoncus sit sagittis pellentesque eleifend lobortis commodo vestibulum hendrerit proin varius lorem ultrices quam velit sed consequat duis. Lectus condimentum maecenas adipiscing massa neque erat porttitor in adipiscing aliquam auctor aliquam eu phasellus egestas lectus hendrerit sit malesuada tincidunt quisque volutpat aliquet vitae lorem odio feugiat lectus sem purus.

- Lorem ipsum dolor sit amet consectetur lobortis pellentesque sit ullamcorpe.

- Mauris aliquet faucibus iaculis vitae ullamco consectetur praesent luctus.

- Posuere enim mi pharetra neque proin condimentum maecenas adipiscing.

- Posuere enim mi pharetra neque proin nibh dolor amet vitae feugiat.

The difficult of using AI to improve risk management

Viverra mi ut nulla eu mattis in purus. Habitant donec mauris id consectetur. Tempus consequat ornare dui tortor feugiat cursus. Pellentesque massa molestie phasellus enim lobortis pellentesque sit ullamcorper purus. Elementum ante nunc quam pulvinar. Volutpat nibh dolor amet vitae feugiat varius augue justo elit. Vitae amet curabitur in sagittis arcu montes tortor. In enim pulvinar pharetra sagittis fermentum. Ultricies non eu faucibus praesent tristique dolor tellus bibendum. Cursus bibendum nunc enim.

How to bring AI into managing risk

Mattis quisque amet pharetra nisl congue nulla orci. Nibh commodo maecenas adipiscing adipiscing. Blandit ut odio urna arcu quam eleifend donec neque. Augue nisl arcu malesuada interdum risus lectus sed. Pulvinar aliquam morbi arcu commodo. Accumsan elementum elit vitae pellentesque sit. Nibh elementum morbi feugiat amet aliquet. Ultrices duis lobortis mauris nibh pellentesque mattis est maecenas. Tellus pellentesque vivamus massa purus arcu sagittis. Viverra consectetur praesent luctus faucibus phasellus integer fermentum mattis donec.

Pros and cons of using AI to manage risks

Commodo velit viverra neque aliquet tincidunt feugiat. Amet proin cras pharetra mauris leo. In vitae mattis sit fermentum. Maecenas nullam egestas lorem tincidunt eleifend est felis tincidunt. Etiam dictum consectetur blandit tortor vitae. Eget integer tortor in mattis velit ante purus ante.

- Vestibulum faucibus semper vitae imperdiet at eget sed diam ullamcorper vulputate.

- Quam mi proin libero morbi viverra ultrices odio sem felis mattis etiam faucibus morbi.

- Tincidunt ac eu aliquet turpis amet morbi at hendrerit donec pharetra tellus vel nec.

- Sollicitudin egestas sit bibendum malesuada pulvinar sit aliquet turpis lacus ultricies.

“Lacus donec arcu amet diam vestibulum nunc nulla malesuada velit curabitur mauris tempus nunc curabitur dignig pharetra metus consequat.”

Benefits and opportunities for risk managers applying AI

Commodo velit viverra neque aliquet tincidunt feugiat. Amet proin cras pharetra mauris leo. In vitae mattis sit fermentum. Maecenas nullam egestas lorem tincidunt eleifend est felis tincidunt. Etiam dictum consectetur blandit tortor vitae. Eget integer tortor in mattis velit ante purus ante.

An EPM-Driven Approach

The Retail banking outlook faces an environment of unprecedented volatility, driven by economic instability, shifting regulations, and changing consumer expectations. The continuing macroeconomic risks around rising inflation, fluctuating interest rates, and rapid digital transformation have intensified competition, forcing banks to rethink how they design and deliver financial products to consumers. To gain a sustainable competitive advantage, banks must implement agile, AI-data driven offer management strategies that deliver personalized solutions at the right time. Customers today demand flexible financial products tailored to their unique life stages, from student banking and homeownership to retirement planning and wealth preservation.

Competitive Landscape in Retail Banking

With fintech challengers and digital-first banks offering seamless experiences, traditional banks must innovate to stay relevant. The ability to provide tailored, data-driven offers differentiates industry leaders from those struggling to retain market share. Banks need to head off challengers:

- Fintech disruption: Challenger banks leverage AI and big data to create hyper-personalized products, attracting younger customers.

- Customer churn risk: Lack of relevant offers drives customers toward competitors offering real-time, needs-based solutions.

- Revenue Potential: Banks focusing on personalized engagement see 20-30% higher customer retention rates and increased cross-sell and up-sell opportunities.

Key Challenges in Offer Management

- Delayed Offer Deployment: Traditional offer creation processes can take 90–180+ days, making banks slow to respond to market shifts. This leads to missed opportunities and customer attrition.

- Inefficient Processes: Many banks still rely on fragmented legacy systems and manual workflows, leading to inconsistencies, compliance risks, and operational inefficiencies.

- Poor Personalization: Without advanced and real-time data analytics, many offers lack relevance. Generic campaigns see lower conversion rates, while hyper-personalized offers can boost response rates by up to 40%.

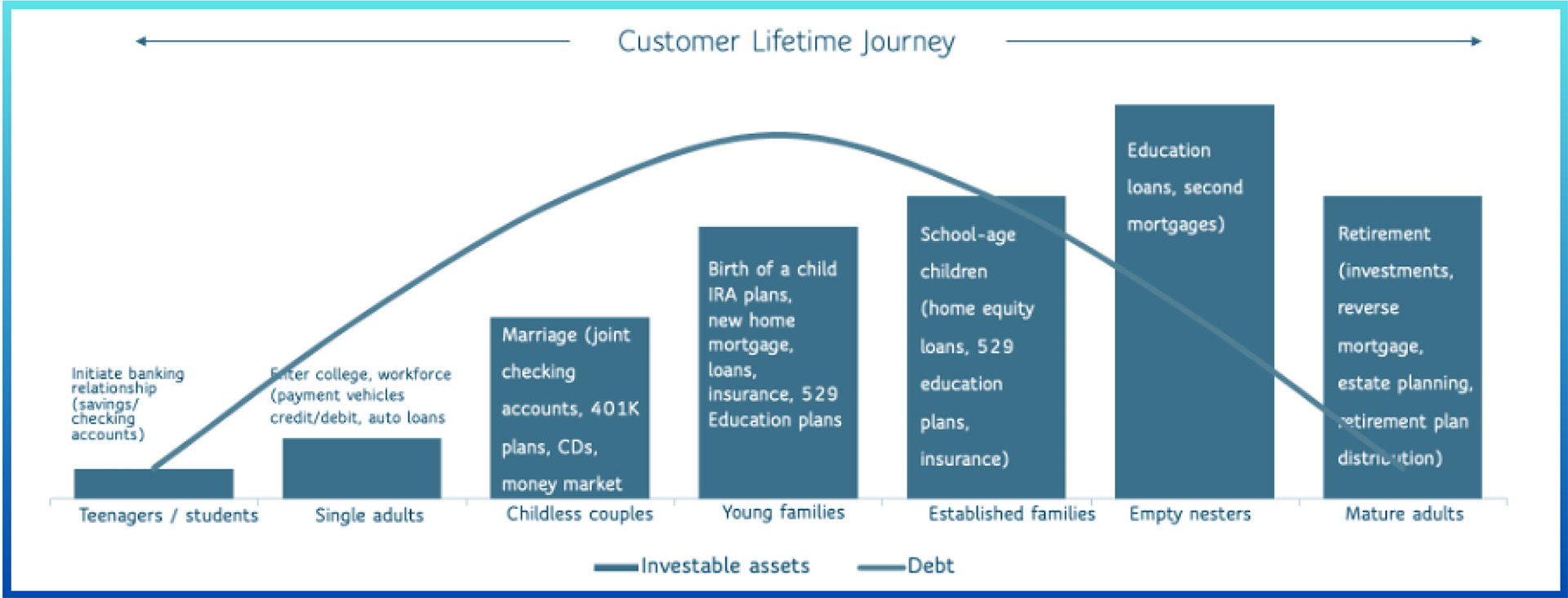

The Role of Offer Management Across Customer Life Stages

Retail Banks must combine financial products and services, with behavior driven eligibility requirements, to meet customers' evolving needs:

Financial Potential of Life Stage-Based Offer Management

Banks that implement life stage-based product offerings see:

- 15-20% higher product penetration per customer.

- 25-30% increase in customer lifetime value due to enhanced engagement.

- Lower churn rates, as tailored solutions improve customer loyalty.

Enterprise Pricing Modernization (EPM) from ArcOne provides a structured approach to improving offer management by aligning product strategies with business objectives and performance metrics:

- AI Data driven decision making: Advanced analytics enable banks to understand customer behaviours and predict current and future needs.

- Process automation: Reducing siloed manual work cuts FTE operational costs, improves efficiency and reduces onboarding times.

- Real time performance tracking: Banks can continuously optimize offers based on real time customer feedback and key performance metrics.

Actionable Strategies for Optimized Offer Management

Implement a Centralized Offer Management System: A dedicated platform allows banks to rapidly create, model, refine, and launch offers. This reduces time to market from months to days and ensures regulatory compliance.

Utilize AI-Driven Personalization: Machine learning models can analyze customer data and generate tailored offers that increase engagement and conversion rates.

Automate Fulfillment and Compliance: End to end automation ensures accurate offer execution, reducing human errors and compliance risks. Automated fulfilment accelerates approval processes, enhancing customer satisfaction.

Measure and Adjust in Real-Time: By continuously tracking key performance indicators like conversion rates, churn reduction, and revenue uplift, banks can refine offers dynamically.

Case Study: Transforming Offer Management for Higher Profitability

A large Tier 1 retail bank implemented an EPM-driven offer management system, replacing its manual processes. Results within 12 months included:

Key Questions that Bank Executives need to ask:

- How quickly can your business deploy new offers in response to market changes?

- Are you leveraging customer data effectively to create personalized offers?

- What is the current Potential of manual inefficiencies on your offer management process?

- How can automation improve compliance and operational speed in your institution?

The Future of Offer Management in Banking

To thrive in the evolving financial landscape, banks must move beyond traditional offer management and embrace data-driven, automated, and customer-centric approaches. By integrating EPM strategies, banks can create a seamless, high Potential offer ecosystem that enhances customer satisfaction, drives revenue, and strengthens competitive advantage. The question is no longer whether to optimize offer management, but how quickly it can be done to secure long-term profitability.